Introduction

What services do we want and expect government to provide? How do we want and expect government to fund and pay for those services?

Eternal questions.

And—let’s face it—no matter how much we might like those government-provided services to be free, they’re not. And cheap? There’s wisdom in the proverb, “You get what you pay for.”

Each of us will have different points of view on these eternal questions. Some will want government to do a lot; others, only the bare minimum. Some will happily contribute their own money (in the form of taxes) to help government fund services; others will rabidly resist giving government a single dollar.

All these positions have various valid points. As citizens in a democracy, where we’re all in the same mess together, these questions are important for each of us to consider and understand. They’re also enormous in both breadth and depth.

In this article, we will zoom in and focus on the question of how we pay for government. We’ll zoom in more and focus specifically on city government in Manchester. We won’t consider federal or state taxes, just city property taxes. And we’ll zoom in further and look at Manchester’s tax cap, which is an attempt to control how fast our property tax rate increases. That’s a lot of zooming in, but the city’s property tax cap is an important issue that looms large in local government.

Quick History

In various parts of the U.S., tax caps have been enacted to slow the rise of taxes, especially property taxes. Supporters see them as a way to limit sudden tax increases and restrain government growth. Opponents argue that such caps starve local services like schools, roads, and public safety; that they merely shift tax burdens elsewhere; and that they restrict the flexibility of local government in handling future issues.

Some examples include:

- California’s Proposition 13, enacted in 1978

- Massachusetts’ Proposition 2 1/2, enacted in 1980

Other states having property tax caps include: New York, New Jersey, Washington, Colorado, Oregon, and Utah.

In New Hampshire, state law allows towns and cities to adopt limits on spending or tax increases. For a city (or a town with a town council form of government) the charter may be amended to limit annual increases in the amount raised by taxes in the budget. The limit must be overridable by a supermajority vote established in the charter. (Note that state law explicitly treats cities and towns differently.)

Manchester’s charter amendment to allow a tax cap was passed by voters in 2009, but complications caused it to be declared invalid by NH’s Supreme Court in 2010. Legislative adjustments in 2011 led to it being retroactively authorized. The city then presented voters with specific tax cap language which they passed in 2011, with 7,203 votes in favor, and 4,991 votes against.

Total votes cast were 12,194, or 10.47% of the city population at that time. The number of votes in favor represented 6.19% of the population. Yes, less than 7% of Manchester’s population cast a vote in favor of this law that all of Manchester now lives with.

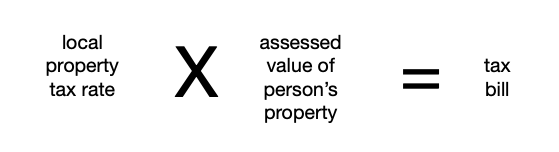

Calculating a City Property Tax Bill

Generally, a Manchester property owner’s tax bill is calculated by

- taking the local property tax rate

- multiplying that by

- the assessed value of the owner’s property

Or:

This means that there are TWO things that can raise (or lower) your tax bill.

- Changes to the assessed value of your property. This may happen because of a kitchen remodel, or because of a state-required revaluation every five years, or for other reasons.

- Changes to the tax rate. This will happen in the latter half of every year when final tax rates for the City of Manchester are set by the New Hampshire Department of Revenue Administration, as required by state law RSA 21 J:35.

The above tax calculation results in two bills from the city to the property owner. In Manchester, these bills are mailed twice per year. The first (or preliminary) bill is generated in May and uses data from the previous year to approximate half of the bill’s total value. Payment is usually due on July first.

The second (or final) bill is typically mailed in October. It reflects to actual tax rate set for the current year, and also many other values that could only be approximated earlier in the year, and will credit the amount already paid toward the preliminary bill. It is usually due on December first.

Interest will be charged on late payments. Bills remaining unpaid for significant periods will trigger tax lien procedures.

Changes to Your Property Value

There are many things that can affect your property value, causing it to rise or fall. Following are some examples.

- Citywide Revaluation: This is required by NH law every five years. In Manchester, they have occurred in 2011, 2016, 2021, and the next will happen this year, 2026. They may include physical home inspections. This will also include examination of comparable home sale data.

- Renovations or additions to your home – Addition of new rooms, Finished basements, New garage, Kitchen remodels, Bathroom upgrades, Addition of decks or pools, Addition of Accessory Dwelling Unit

- New construction

- Property deterioration or damage – Fire, Flooding, Demolition, Deferred maintenance

- Changes in use, such as – From residential to commercial, From single-family to multi-family, From owner-occupied to rental

- Market conditions – Rising sale prices nearby, Changes to neighborhood desirability, School perceptions, Crime trends

- Correction of errors – Square footage, Lot size, Condition rating

How to Challenge an Assessment

In Manchester if you believe your assessed property value is wrong, you can contact the Assessing Department to review any possible errors in your assessment. You can file a formal tax abatement request. Note these must be done by March 1 following a final tax bill. You may need evidence such as information about comparable sales, appraisals, and photographs. For more info, see here.

Types of Tax Caps

All types attempt to restrict how fast tax bills can change. No one wants to get surprised by an unanticipated larger bill. Different kinds of property tax caps focus on different elements of the above tax bill equation.

Rate caps – place a ceiling on the property tax rate, in terms of dollars of tax owed per thousand dollars of assessed property value.

Assessment caps – limit the annual increase in the assessed value of any individual’s property. Of course actual prices of properties sold may stubbornly refuse to obey legislation.

Total levy caps – the most restrictive type of cap, limit the annual increase in a locality’s total property tax revenue.

Manchester’s charter imposes a cap on city expenditure growth and also on growth of property tax revenue.

How Tax Caps Affect Public Services

Caps affect all city services financed by property taxes, unless explicitly excluded in legislation. Property tax revenues mostly pay the salaries of local government employees such as teachers, police officers, and firefighters. In many communities, they also pay for road and school construction, park maintenance, human services, and other items. The costs of all these items rise from year to year due to inflation, population growth, and sometimes other factors, such as changes in state law, or changes in the mix or quality of services needed to remain competitive with other jurisdictions. Localities need to offer salaries that are competitive with the private sector, and other nearby communities, in order to attract qualified workers. If neighboring towns are paying their police officers much more, then your town may need to increase its police salaries to retain talented law enforcement personnel. Obviously that will impact the budget.

Changes to the local business environment also have an impact. If many employers come into a city, wages may rise, meaning the city will have to pay higher salaries to retain skilled police, firefighters, etc.

Manchester’s tax cap explicitly does not apply to:

- Enterprise Funds (such as the Airport, Environmental Protection, Parking, Water Works)

- Central Business Service District

- Amounts payable in connection with municipal bond obligations, whether issued for school or municipal purposes

Arguments For and Against Tax Caps

Proponents may argue property tax caps will force localities to provide services more cost-effectively, or to eliminate services that are not needed. Opponents contend that caps are more likely to force localities to cut necessary services. As an example they point to California, where education, health care, transportation, and other public services all have declined dramatically since the state adopted a tight property tax cap (Proposition 13) in 1978. California’s school system, formerly one of the best in the country, became one of the worst.

Similarly, some Massachusetts towns have had to lay off school and municipal employees (including fire and police), freeze wages, and close town libraries and senior centers in order to comply with Proposition 2 ½, that state’s severe property tax cap.

Mitigating the Impact of Tax Caps

Localities can mitigate the impact of a tax cap by voting to override it. (Most existing caps, like Manchester’s, allow temporary or even permanent overrides.) Override campaigns tend to be highly politicized.

Moreover, override systems have proven to be inequitable. More affluent communities pass overrides much more often than lower-income communities. This can exacerbate disparities across a state in education and other important services, leaving poorer communities even worse off relative to their wealthier counterparts.

Manchester’s Tax Cap

In simple language, the legislation describes rules to limit how much city property tax revenue (money coming in) can grow, and also to limit how much city expenditures (money going out) can grow. These rules are depicted in a chart below. For the upcoming fiscal year, if either (A) the city’s property tax revenue, or (B) the city’s total expenditures, will need to exceed the calculated limit, then the Board of Mayor and Aldermen must vote to override (or “break”) the tax cap.

When these limits to growth are encountered, the limit on revenue growth is nearly always hit before the limit on expenditure growth. The process of calculating the limit on revenue growth is depicted below. (To calculate the limit on expenditure growth, you follow the same process, but substituting total expenditures in place of property tax revenues.)

Note that in describing this process, anywhere we speak of the Consumer Price Index, we are specifically referring to the CPI-U, or Consumer Price Index for All Urban Consumers. More info here.

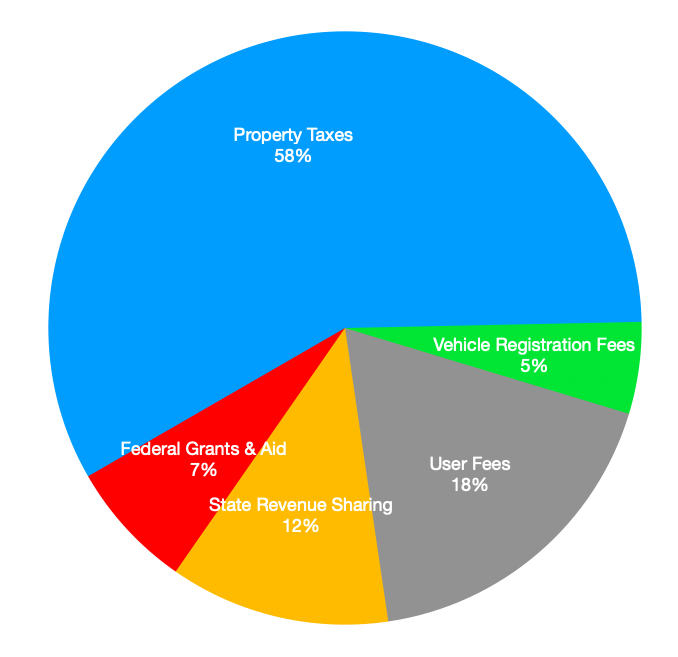

Note that property taxes are merely ONE of several sources of revenue to the city of Manchester. They are the largest one at about 58% of the total, but they are not the only one. See below chart. Non-property-tax revenue sources are not affected by the tax cap.

So, even if property tax growth is limited by the city’s tax cap, other sources of revenue, approximately 42%, remain unaffected by the tax cap. However, other factors may cause those revenues to rise or fall, and those factors are usually beyond the control of the city.

Other sources of revenue include:

- Motor Vehicle Registration fees;

- User Fees and Service Charges, such as water rates and sewer charges; building permits, planning or zoning applications, inspection fees;

- State Revenue Sharing such as Meals and Rooms Tax Distribution, Highway Block Grants, Education Aid, Grants related to Housing, Environmental programs, or Transportation;

- Federal Grants and Aid, such as Community Development Block Grants (CDBG), HUD housing funds, Transit funding, ARPA programs.

Note that Federal grants are awarded for a specific purpose and must be accounted for separately. For example, if the City receives a $1 million federal grant for affordable housing, those funds are placed in their own project account and are not commingled with other resources. Only qualifying expenditures are charged to that grant. Many state funds must be treated in a similar manner.

Finally, it should be noted that, by state law RSA 21 J:35, final tax rates for the City of Manchester are set by the New Hampshire Department of Revenue Administration.

The full and complete language of Manchester’s tax cap legislation is a one-and-a-half page PDF available here.

Example

As an example, let’s calculate how much the city property tax revenue can increase next year, using data we have right now.

- In 2024, the CPI-U rose over the previous year’s value by 3.4%.

- In 2025, the CPI-U rose over the previous year’s value by 2.3%.

- In 2026, the CPI-U rose over the previous year’s value by 3.8%.

The average is ( 3.4 + 2.3 + 3.8 ) / 3 = 3.17%.

So the city’s budget amounts for this year can grow over last year’s by 3.17%. For every $100 dollars the city collected in property tax, or spent, last year, in the coming year it can collect in property tax, or spend, $103.17.

How to think about that?

Is it reasonable? Compare it to your own personal experiences. When you go to Staples for pens or paper, or when you go to Home Depot to buy lumber or an air conditioner, do you expect to pay roughly three percent more than last year? If you spent $100 at Target last year, would you expect those same items to cost $103.23 today? Or might they cost even more? That’s what this boils down to.

Note we did not use groceries in these examples. Prices for food often rise at rates different than non-food items. And most city expenditures do not involve food (with the notable exception of school cafeterias.) So we avoided food in this example.

There’s nothing magic about these numbers. The Board of Mayor and Alderman can vote to raise property taxes more than the tax cap dictates, and/or to spend more funds than the cap dictates. Since the cap was created, it has been overridden slightly fewer than half of the years it’s been in effect. So overriding is not uncommon. Think about your own life, and your own home. Some years are good, and you may get an unexpectedly fat tax refund check. Other years, you discover you need a new roof.

Overrides

With the equations and calculations outlined above, much approximating is involved until late in the year. Furthermore, unanticipated needs are bound to pop up in the operations of a city of 116,000 people. So the charter amendment lays out a procedure to override the tax cap. Some might even say that the tax cap was designed and expected to be overridden frequently, explicitly in order to make budgetary discussions and decisions transparent and documented.

With a two-thirds vote, the Board of Mayor and Aldermen may override the tax cap, allowing the city to bring in and/or spend more money. This could become necessary when some city costs have risen faster than the average of the changes to the Consumer Price Index for All Urban Consumers (CPI-U) over the last three calendar years.

For example, inflationary spikes in the wake of Covid-19. Or when decades-old infrastructure needs to be repaired or replaced. Or when non-tax revenue takes a fall, but expenditures continue on smoothly.

Note that Manchester’s tax cap limits both revenues and expenditures. However, when the tax cap is overridden by a vote of the Board of Mayor and Aldermen, then both revenues and expenditures are in play and may be assigned values which exceed the limits that would otherwise be in effect.

Tax Relief in Manchester

Manchester offers several forms of property-tax relief, most of which are authorized by state law and administered through the City’s Assessing Department. These programs are designed to reduce taxes for qualifying homeowners or allow taxes to be deferred.

Below are some of the forms of relief available. Click the links for more info.